Helping you understand how much risk you are prepared to accept when making an investment decision.

The following process is designed to help you understand how much risk you are prepared to accept when making an investment decision. It is not trying to place you, as a person, in a particular risk category, but rather guide you on the amount of risk you might want to take if you are looking at a specific investment decision. It also aims to help you understand how an investment matched to this level of risk might behave.

The process will bring you through five stages:

1. RISK

2. A FEW QUESTIONS

3. VALIDATION

4. INVESTMENT SUITABILITY

5. REPORT

1. Risk

There are a number of different types of risk you need to consider before making an investment. Here are just a few to think about.

This is the first thing most people think about when they consider investment risk. The risk that you may lose some of your intitial investment. How would you feel if this happened?

Although your initial investment may be intact, the growth on it may not have kept pace with inflation.This means you would be able to buy less with it at the end of the investment term than you could at the start.

You may invest in a product which provides a guarantee. Counterparty Risk is the risk that the institution providing the guarantee isn’t able to honour its promise.

This risk also applies to funds which invest in bank deposit accounts, corporate or government bonds.

You might plan to invest for a long time but your circumstances can change unexpectedly. You should take into account that not all investments are easy to get out of early. Some may not give you the full value you might expect, others may not allow you access at all.

This is the “all your eggs in one basket” risk. If too much of your wealth is concentrated in too few assets, or asset types, you are increasing the negative impact it could have on you if anything happens to one of them.

2. A few questions

We are now going to ask you 5 simple questions so we can understand a bit more about your investment experience and attitude to risk. The questions will ask you about:

- Your investment experience

- The importance of this investment to you

- Your attitude to the safety of this investment

- The risk and return expectations

- Your attitude to short term loss

3. Validation

Based on your answers to the questions posed in Step 2, your Financial Advisor will suggest a level of risk he or she thinks is most appropriate for your needs.

Although an investment’s risk can change over time, this tool can give you a feel for the types of return an investment may demonstrate if its risk level stays the same. Your advisor will bring you through possible ranges of returns for the level of risk they think most appropriate. You can then decide if this matches what you had in mind, or you can look at alternative risk options.

4. Investment Suitability

There are a number of different types of risk you need to consider before making an investment. Here are just a few to think about.

We use the European Securities and Markets Authority (ESMA) risk scale. This scale is widely used throughout the investment industry and uses volatility to classify different investments along a 7 point risk scale. Volatility is a measure of how much an investment’s value goes up or down over a given time.

Based on your responses, a Very Conservative investment might be suitable for your needs.

You are likely to need an investment which gives some form of capital protection. Your Financial Broker or Adviser will talk to you about possible options.

When looking at products which provide capital protection you need to be particularly aware of:

- Counterparty Risk

- Inflation Risk

- Liquidity Risk

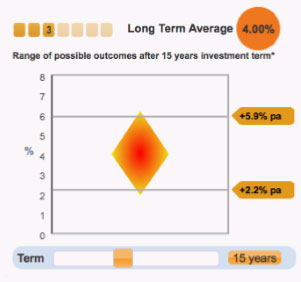

A diversified investment will have a mix of defensive and growth assets. This mix will determine how risky the fund is and what would be a reasonable long term growth potential.

The more growth assets held the riskier the investment but the higher the long term growth potential.

A fund with a risk rating of 3 is likely to have a significant weighting to defensive assets. Based on Society of Actuary guidelines, 4.00% p.a. would be a reasonable long term average expected return for such an investment.

Investment Suitability – Short Term Volatility

Although it is reasonable to have a long term average expected return, the returns in any one year are going to be higher or lower than this. Depending on the expected volatility of the investment, it is possible to estimate a range of annual outcomes which would be deemed ‘normal’ for that type of investment. The graphic opposite illustrates the likely spread of annual returns. You will see that most of the time returns will be around the long term expected average. However, more extreme outcomes are probable.

*This assumes 95% probability, more extreme outcomes are possible.

Investment Suitability – Long Term Volatility

Over time your investment will have both good and bad years. The longer your investment period the predicted range of annual returns will get closer to the long term average.

However, you should also note the impact of compounding. A small annual profit or loss, over a long period of time, can have quite an impact on the value of your investment.

*This assumes 95% probability, more extreme outcomes are possible.

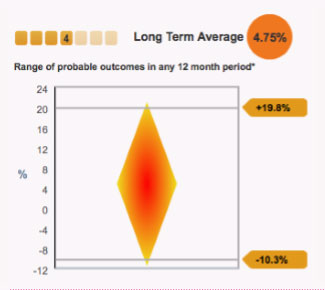

A diversified investment will have a mix of defensive and growth assets. This mix will determine how risky the fund is and what would be a reasonable long term growth potential. The more growth assets held the riskier the investment but the higher the long term growth potential.

A fund with a risk rating of 4 is likely to have a good balance between defensive and growth assets. Based on Society of Actuary guidelines, 4.75% p.a. would be a reasonable long term average expected return for such an investment.

Investment Suitability – Short Term Volatility

Although it is reasonable to have a long term average expected return, the returns in any one year are going to be higher or lower than this.

Depending on the expected volatility of the investment, it is possible to estimate a range of annual outcomes which would be deemed ‘normal’ for that type of investment. The graph opposite illustrates the likely spread of annual investment returns. You will see that most of the time returns will be around an expected long term average. However, more extreme outcomes are probable. *This assumes 95% probability, more extreme outcomes are possible.

Investment Suitability – Long Term Volatility

Over time your investment will have both good and bad years. The longer your investment period the predicted range of annual returns will get closer to the long term average. However, you should also note the impact of compounding. A small annual profit or loss, over a long period of time, can have quite an impact on the value of your investment.

*This assumes 95% probability, more extreme outcomes are possible.

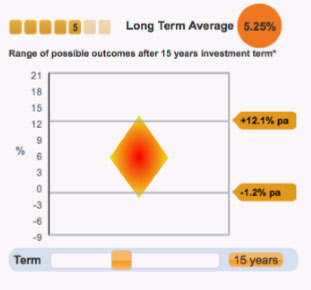

A diversified investment will have a mix of defensive and growth assets. This mix will determine how risky the fund is and what would be a reasonable long term growth potential. The more growth assets held the riskier the investment but the higher the potential for long term growth. A fund with a risk rating of 5 is likely to have a higher weighting in growth assets. Based on Society of Actuary guidelines, 5.25% p.a. would be a reasonable long term average expected return for such an investment.

Investment Suitability – Short Term Volatility

Over time your investment will have both good and bad years. The longer your investment period, the range of annual returns predicted will get closer to the long term average. However, you should also note the impact of compounding. A small annual profit or loss, over a long period of time, can have quite an impact on the value of your investment. *This assumes 95% probability, more extreme outcomes are possible.

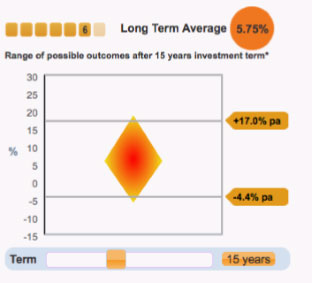

A diversified investment will have a mix of defensive and growth assets. This mix will determine how risky the fund is and what would be a reasonable long term growth potential.

The more growth assets held the riskier the investment but the higher the long term growth potential.

A fund with a risk rating of 6 is likely to have a significant weighting of growth assets. Based on Society of Actuary guidelines, 5.75% p.a. would be a reasonable long term average expected return for such an investment.

Investment Suitability – Short Term Volatility

Although it is reasonable to have a long term average expected return, the returns in any one year are going to be higher or lower than this. Depending on the expected volatility of the investment, it is possible to estimate a range of annual outcomes which would be deemed ‘normal’ for that type of investment.

The graph opposite illustrates the likely spread of annual investment returns. You will see that most of the time returns will be based on the long term expected average. However, more extreme outcomes are probable. *This assumes 95% probability, more extreme outcomes are possible.

Investment Suitability – Long Term Volatility

Over time your investment will have both good and bad years. The longer your investment period the predicted range of annual investment returns will get closer to the long term average. However, you should also note the impact of compounding. A small annual profit or loss, over a long period of time, can have quite an impact on the value of your investment. *This assumes 95% probability, more extreme outcomes are possible.

5. Recommendation

Your appetite for risk is one of the inputs into which investment is suitable for your current needs. Your Financial Broker or Adviser will conduct a full Financial Fact Find with you before recommending a specific fund or funds. The output from this Investment Suitability Process should be read in conjunction with your Financial Broker or Adviser’s recommendation.

It is important to be aware that there are a number of different ways to look at assessing appetite for risk and it is not an exact science.

This process does not take into account all your personal circumstances and therefore the calculations may not be appropriate to your personal circumstances.

You should not rely solely on this process to make an investment decision. In all cases we recommend that you consult a Financial Broker or Advisor who will conduct a full financial review and fact-find with you and advise you accordingly.

The calculations provided by the Friends First Investment Suitability Process are for general illustration purposes only, based on the limited inputs you have given and assumptions made. Although Friends First endeavours to ensure that this ‘Investment Suitability Process’ is accurate, we cannot guarantee it is free of errors or suitable for any user’s intended purposes. To the extent permitted by law, under no circumstances will Friends First be liable for any investment loss or damage caused by a user’s reliance on information obtained by using this process.

Latest News

Auto Enrolment Employer Guide

Auto Enrolment Employer Guide The Auto Enrolment Retirement Savings System Act 2024 was signed into law by the President on the 9th of July 2024. The Act provides for the setting up of the [...]

2025 Value of Advice Report

2025 Value of Advice Report Brokers Ireland is delighted to publish the 2025 Value of Advice report which illustrates the significant impact and value that professional financial advice delivers through the expertise of Financial [...]

Brokers Ireland Newsletter – 27 August 2021

The benefits of using a financial adviser. Brokers Ireland recently published the latest research showing how much better off financially and mentally consumers are for using a financial adviser such as OBI. Remarkably, the [...]